As of 7 March, my updated view (subject to wide change). COVID is worse than seasonal flu by 10x - 20x and Pandemic flu (Swine Flu) by 4x, but the worse case panic (eg Spanish flu, 1918 )is overstated because treatment is likely (60% chance IMO) coming in 6 months and there is decent chance (but not overwhelming) that hot weather will slow progression (although not completely halt). So reality lies between, “don’t panic, it’s flu” and “panic, it’s Spanish ‘flu pandemic”.

Risk is around healthcare services being swamped by exponential growth of critical cases before treatment is approved. Medium-term (1-2 year), est of 50% infection rate is plausible. 6-12 months for treatment (80% chance, my view; remdesivir my top choice, baricitinib others possible). 24 month+ for vaccine (70% chance, timing a challenge).

The political fall out is unknown. The US has been unexpectedly poor. South Korea and Singapore have been (expected?) good. China after a (arguably) slow start has since performed strongly. UK response (as judged by testing seems OK but NHS beds already stretched over winter.

The second order economic impact also quite varied, base case is a 6 - 12 month slow down (50% recession chance) with recovery thereafter, but with downside risk from US particularly given impact to small business. Markets to remain volatile. (OECD downgraded World GDP from 2.9% to 2.5% on containment scenario, but would fall to 1.5% under a non-containment scenario).

Good single source data: World In Data

Useful Dashboard from @avatorl

Further round up below.

Present

-WHO report and collections of COVID resources

-Prediction markets

-My notes from healthcare conference

-health/economics/social/market impacts

Future

-what to do about future pandemics

-incentives for innovation and stores of knowledge

-dissuade state-appropriation, but increase state capacity

I thought I’d put my growing collection of COVID thoughts in one place. There is much expert information on the web so I would point you to that. I have studied healthcare investing for 20 years, but the still puts me in a distinctly amateur category. My major contribution here is to think about what to do about the medium to long term, as it looks highly like there will be recurring pandemics (as there have been before). But before getting to that have a look at a collection of papers sources to start.

Current Resources

On what to do this is WHO: https://www.who.int/emergencies/diseases/novel-coronavirus-2019/advice-for-public. (Mostly you can find advice on this readily on the web)

This WHO report: Report of the WHO-China Joint Mission on Coronavirus Disease 2019 (COVID-19) is pretty much (as of early March) one of best details one stop information sources.

“…In the face of a previously unknown virus, China has rolled out perhaps the most ambitious, agile and aggressive disease containment effort in history. The strategy that underpinned this containment effort was initially a national approach that promoted universal temperature monitoring, masking, and hand washing. However, as the outbreak evolved, and knowledge was gained, a science and risk-based approach was taken to tailor implementation. Specific containment measures were adjusted to the provincial, county and even community context, the capacity of the setting, and the nature of novel coronavirus transmission there.

…. China’s bold approach to contain the rapid spread of this new respiratory pathogen has changed the course of a rapidly escalating and deadly epidemic. A particularly compelling statistic is that on the first day of the advance team’s work there were 2478 newly confirmed cases of COVID-19 reported in China. Two weeks later, on the final day of this Mission, China reported 409 newly confirmed cases. This decline in COVID-19 cases across China is real…”

But

“…COVID-19 is spreading with astonishing speed; COVID-19 outbreaks in any setting have very serious consequences; and there is now strong evidence that non-pharmaceutical interventions can reduce and even interrupt transmission. Concerningly, global and national preparedness planning is often ambivalent about such interventions. However, to reduce COVID-19 illness and death, near-term readiness planning must embrace the large-scale implementation of high-quality, non-pharmaceutical public health measures. These measures must fully incorporate immediate case detection and isolation, rigorous close contact tracing and monitoring/quarantine, and direct population/community engagement.”

Characteristics of and Important Lessons From the Coronavirus Disease 2019 (COVID-19) Outbreak in China. Summary of a Report of 72 314 Cases From the Chinese Center for Disease Control and Prevention (Feb 24)

Also very good overview of China situation. JAMA article: https://jamanetwork.com/journals/jama/fullarticle/2762130

There are many non-symptom carriers (see notes below from HC conf). But NEJM letter shows it by case study: https://www.nejm.org/doi/full/10.1056/NEJMc2001899

My own notes on COVID from a recent healthcare conference are here:

Notes on #COVID from Healthcare Conference (Boston).

Prof. Suggests many (>50% ?) of ppl at conference likely already exposed.

40 - 60% eventual exposure rate for US population plausible (and in his view likely but timing unknown).

(Based on Washington State and several papers) seems many ppl show no/mild symptoms, many still have virus post-symptoms, unknown if still shed virus post symptoms/asymptomatic but likely. Many likely undetected so death rate still unclear. Info. v. Fluid. (Lots of papers suggest this, also suggestion two strains already in circulation, one more virulent)

Good news: Children seemingly not at higher risk of death.

Bad news: Elderly, and already ill, at higher risk.

Unknown but possible:

-if summer/heat will kill off virus (to what extent, as it is heat sensitive; but it’s novel)

-if mutation and numbers make this another seasonal infection on going (hiigh uncertainty, but mosre seem to be leann this way)

US hosp. Could be overwhelmed (mixed views in room, decent votes for stretched, decent votes for very overwhelmed).

Future cures/vaccines: Possible treatments in 2020 (not advice, but Gilead’s Remdesivir on treatment, Incyte/Lilly’s baricitinib; Moderna on speed of its novel vaccine) plus quite a few more.

Commercial vaccines not likely for 18-24 months+, but from 2022 vaccines possible + maybe routine. Treatment could be in 2020.

Large debates on exponential compounding (or not) and views on risk plus uncertain second order impacts on business, supply chains, remote working, politics etc. Plus observations that if we can manage for COVID can we manage for eg. Air pollution or other big killers.

Now for more quirky resources:

A daily newsletter summarising developments: https://cronyclecovid19.substack.com/

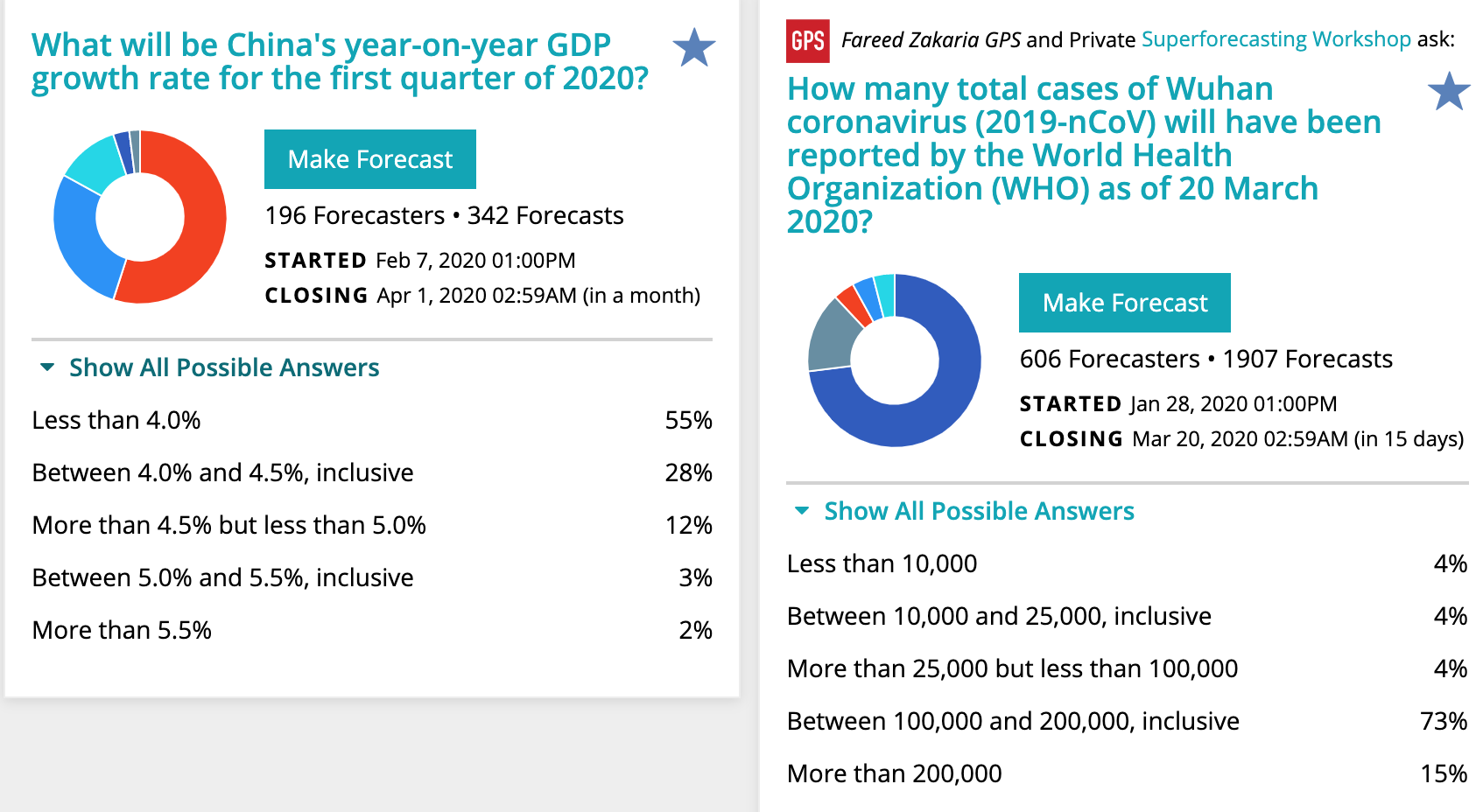

This GJ Open Prediction market on COVID. I am participating (and along with other questions). My Brier score current 0.7 vs crowd at 0.8 (so I’m 0.1 better - scale is 0 to 2), but some of the questions very hard!

It really focuses the mind if you try and actively predict and record why you are predicting an item. https://www.gjopen.com/challenges/43-coronavirus-outbreak

In that worth looking at Tyler Cowen’s column on exponential growth forecasting (and compounding) vs base rate effects. https://www.bloomberg.com/opinion/articles/2020-03-03/how-fast-will-the-new-coronavirus-spread-two-sides-of-the-debate

And my own previous blog on how to forecast drug success rates.

Future

Very broadly there are a few interlinked impacts to think about.

Public Health impacts

Economic Impacts

Social Impacts (cultural change, and interlink with economic)

(Maybe less important but who knows) Financial market impacts

My sense is that people in the US thought the US system would have handled this better (especially the testing, which is behind). And while the population in China are upset and emotional, the WHO have come down positive on China’s handling, and looks like South Korea and Singapore also faring well. The end game looks like 50%+ of US (and world) eventual infection. Death rates are always difficult to put in context - as most people had no idea that season flu was such a big killer, and most completely underestimate the killer effects of eg. Air pollution.

Still - my *amateur* sense is that this is broadly in the 2009 swine Flu pandemic bucket. This was:

“…estimated that 11–21% of the then global population (of about 6.8 billion), or around 700–1400 million people contracted the illness - About 150,000–575,000 fatalities..” see https://www.cdc.gov/flu/spotlights/pandemic-global-estimates.htm

So if COVID is going to hit about 50% - that’s about 4bn people (or 4x swine flu), with an unknown death rate.

If the range is 0.01% to 3% (worse case) that’s about 400,000 to 140m deaths.

The Economist put it:

A broad guess is that 25-70% of the population of any infected country may catch the disease. China’s experience suggests that, of the cases that are detected, roughly 80% will be mild, 15% will need treatment in hospital and 5% will require intensive care.

So it’s in line.

Set against that is if drugs we have are effective and when (and there’s good reason to believe that we have some effective treatments which we are testing now) and longer term how quickly we can develop a vaccine.

There is also going to be much scrutiny about capacity in this area.

The above picture is why some are calling for much stricter/organised public health interventions. They argue that flattening the potential exponential growth and extending the time allows for treatments and less stress on health capacity.

Especially it is about 5% of cases in ICU eventually.

(2) China is showing signs of slowly starting a normalising process - from companies I speak to - but it looks like economic impacts from lost work and supply chains etc. will last longer than recent swine flu or SARS. So 6 to 12 months+. A good portion of that doesn’t come back. (eg a shoe maker who makes a shoe a day, is going to lose all those shoe-days) but productivity levels should come back as it has done previously.

So large short term impact, but world recovers. This is essentially the Ray Dalio view (see end) but large uncertainty and caveats. This is mostly because of the intersection with social-politics eg inequality, wroker protection. If people are forced not to work, and they don’t have any safety net then this hits poor people and gig economy people potentially very hard. Lots more possible here to think about.

(3) More lasting could be social impacts. Will we find new ways of working and learning? That actually work for us. Will remote working start to show its worth. How will we think of events?

How will US politics change ? China politics ? Singapore has seemingly strengthened its reputation. Healthcare could rise up the US political agenda and weak economies tend to be no good for incumbent politicians. Will this be bad for Trump?

Does China become restricter or does free speech become easier?

Could this be better for the environment? Air pollution?

Will we travel less for a time? Or even longer?

How successful will our open collaborations be? Will this spur future investment in more healthcare infrastructure and genomic technologies.

Will this cause a re-think of long global supply chains, and spur investment in local supply for food, energy, staples? Does this strengthen localism? Populism?

COVID is going to throw many of these social-political questions open. Especially the intersection with the poor and the healthcare questions in the US.

(4) Markets both debt and equity have displayed volatility as they deal with both emotion and evolving data.

To the extent that they impact funding for businesses (eg capital raising for innovation) and that bear markets are hard on the psyche then they may have an evolving role.

But mostly (from what I see) economists (eg Larry Summers, Jason Furman) have identified fiscal responses as most appropriate. See: https://www.washingtonpost.com/opinions/2020/03/03/how-economic-policymakers-can-respond-growing-economic-shock-coronavirus/

OK. On to my contribution here about the long term and innovation:

Future innovation

Pandemics are very likely (over 90% chance) to occur (again) over the next 50 years and likely over 100 years+ time frames. This pandemic was predicted by pandemic experts.

This is because:

-humans are increasingly interconnected at speed

-the way we treat/breed animals is not changing any time soon

-wet markets and similar not likely to change soon (though I think in eg China there will be a crack down)

-current viruses/germs eg influenza, pneumonias have been around for 1000s years

-virus/germs will constantly mutate

-containment will slow, likely never stop, transmission

I don’t have more room to explain these assumptions but will leave links at the end, but if you don’t accept this premise then you will under-rate what follows

What to do about future pandemics

-cultural learnings eg greetings

-innovation

We can slow transmission and in small cases potentially even stop by a change in cultural norms. We know the behaviours - washing hands, hygiene, don’t shake hands, cough into elbow - but compliance can be greatly improved. This is inexpensive. Still, it is unlikely to stop all future pandemics. It’s worth recommending more strongly. Sanitation has already given use huge gains here and can gives us further gains.

That leaves us with treating pandemics and vaccinating once pandemics start. This is a question of innovation.

Incentivising Innovation

The market arguably has inefficiencies with dealing with i) rare diseases and ii) developing world diseases and iii) diseases that have not occurred, but we can predict are likely to occur.

This is due to those markets being risky and/or commercially small and/or commercially small risk-adjusted (a market might be worth $2bn but at 1% chance of success, $20m risk-adjusted would be of small value).

Policy solutions that have (at least partially) worked have been a) granting longer/extra intellectual protection for rare diseases and b) agreed forward purchasing contracts for developing world diseases.

(a) Has helped areas such as rare genetic diseases, and multiple sclerosis (and other classified rare diseases) in the developed world (mostly) and

b) has helped in malaria and certain other developing world diseases (where commercial markets are smaller) - forward buying by the Gates Foundation amongst others.

Such mechanisms have mostly failed in I) developing new antibiotics against resistant strains, II) certain other developing world diseases, III) pandemics.

One negative factor in this is state appropriation of (mostly) private innovation. Rich countries eg US have been guilty of this as much as poor countries. The US essentially disregarded protection (or threatened to break the patents) on anthrax treatments in seeking to stockpile such medications cheaply. [https://www.wsj.com/articles/SB1003966074330899280 ]

This causes a large disincentive to work on vital areas, if profit-seeking entities will lose out on their R&D development costs for such treatments.

I would propose:

-partial speed up of regulatory response for areas of unmet medical need

-international “state capacity” in anteviral, antiobiotic, mRNA, pandemic research

-forward purchase fund for pandemic vaccines and medications

Partial speed up of regulatory response for areas of unmet medical need

The gold standard in medical research are randomised controlled trials (RCTs). They are costly and slow, but typically generate the most robust results.

For low commercial value areas, RCTs (and previously trials needed before RCT) are too costly for entities to perform give the risk.

But, mostly health regulators will need RCTs before approval of a drug to be able to know the risk/benefit of a medication vs standard of care.

This has led some thinkers (eg Peter Thiel) to argue that regulators need to change or relax standards to allow quicker and more innovation on to the market. The challenge is that this may let onto the market ineffective treatments that cost lives or damage the credibility of the system.

One compromise would be to let medications on to the market where - in a controlled fashion - when there is enough evidence of safety/efficacy but no RCT. A full approval would be contingent on future RCTs being performed in a reasonable time frame else the drug would be with drawn from the market. The drug would also be withdrawn if the RCT fails.

If medications for areas of high unmet need - for instant pandemics or other diseases with limited treatment options - would be released this way, the net benefit would be positive.

Industry would pay for such a faster service, and this could cut drug development time in half.

International/national “state capacity”

Faster regulation alone would not help unless there were medications to test. Given the long and uncertain cycles for viral pandemics, it’s beyond the risk tolerance for many private entities. There are further complications because mutations might mean the plan A vaccine proves to be relatively ineffective and has to be made again under plan B.

However, I believe this is an area where even libertarians or perhaps “state capacity” libertarians might concede a non-private institution or set of institutions might be useful.

Essentially, I would be arguing for a form of Health ARPA where a part of the HARPA is focused on pandemic anteviral research, and antibiotic research and possibly other areas of unmet medical need. This is a sibling idea to the NIH but more targeted at likely pandemics.

If such an organisation had capacity to response quickly to evolving pandemics, then it should be able to share royalties with any other parties needed to scale medications to commercialisation, if it needed private partners to help scale quickly.

There should be positive spillover (cf NIH) in the years when no pandemics occur.

Forward purchase fund for pandemic vaccines and medications

Now (A) We have an organisation that can respond quickly with a new medication, and (B) a regulatory process which can speed through medications for high unmet need (eg pandemic) but how will we pay and keep incentives especially if we need multi-stakeholders to develop the medication.

This is where a forward purchasing fund or contract comes into play. This fund acts as a guarantee that a certain amount will be paid for the innovation in a swift manner.

On the one hand this should give a guarantee to private or other players that the innovation won’t be appropriated for nothing. But, also given that it’s a guaranteed market, and the risk is lower, the price for the medication can be set in a more fair manner especially for poor countries (cf HIV).

This is similar to were the Global fund and GAVI already sit. I do note the US govt has approved funding quickly on COVID, but still better to have it already in place.

Conclusion

Given pandemics will re-occur, we should look to set up capacity to deal with pandemics, regulation that can be swift and responsive and a fund to guarantee a fair price for innovation and set incentives accordingly

Post Script: It turns out Bill Gates haas also written on this topic and he many similar ideas and sources (and talks more about infrastructure build) examples of certain pandemic preparation here. https://www.nejm.org/doi/full/10.1056/NEJMp2003762

On why Pandemics will (re)occur: https://www.worldbank.org/en/topic/pandemics#1