In ESG world, I did a webinar! For those who want to know a slice of what I do during the day – you can see the archive of it here. (free to register) I mention the work of Stian Westlake on intangibles which I’ve blogged about before.

MSCI: On ESG in higher ROIC companies

MSCI: “Among a universe of companies that have generated substantial value for their shareholders over the last decade (Jan. 2007 – Dec. 2017), we found that companies with strong management of industry-specific ESG risks and opportunities outperformed peers with poorer management of those same ESG risks and opportunities over the five year period from Jan. 2013 to Dec. 2017.”

“In this paper we apply an ESG filter to a highly selective universe of 100 companies that have already been screened for value creation as measured by ROIC, economic spread, margins and asset turnover ratio. We found that, over the last five years, companies with higher ESG Ratings exhibited higher average return on invested capital, compared to companies with lower ESG ratings. They were also valued at a premium over their other top performing peers with lower ESG Ratings. …. the main additional value of our ESG ratings did not come from our governance assessment in this case, but rather from how well these firms managed their industry-specific environmental and social risks, which varied considerably across different business models.”

You can download the paper through MSCI here. You can find the co-author Panos Seretis on Linkedin.

Caveats: Not peer reviewed, time frame limited and it has the ROIC-cost of capital framework as the economic value add but still an interesting and useful addition to the body of ESG research.

What are Governance ratings missing?

What are #Governance ratings missing? “Company #culture, sub-board management, alignment with strategy, track record on target delivery and the positives from long-term ownership are all underappreciated when it comes to the criteria used to rate the “G” in “ESG”. Code compliance is a poor proxy for good or bad practice in these areas”

What does the gap between a group’s policy and practice say about its culture?

Is sub-board level management taken into account when scoring governance?

Are the minority risks often associated with family ownership offset by governance positives?

How is the governance of cyber risk assessed?

Culture – How quickly did the company release bad news? Was the impact estimated? Was the market kept updated? How soon was the impact quantified?

Timeliness – Governance is dynamic, and changes are not tied to the annual reporting schedule. How current is the governance view that informs your rating?

Tenure - Has leadership been there long enough to demonstrate performance across business cycles?

Strategy – Are board changes aligned with strategy or is Code compliance the driver?

Good questions and thinking from Paul Marsland (Kepler) in his latest #ESG report: What are #Governance ratings missing? Can link you up if interested.

Inequality. Inevitable? How bad?

Inequality. Does it matter ? “our most fundamental challenge is not the fact that the incomes of Americans are widely unequal. It is, rather, the fact that too many of our people are poor .” Princeton philosopher Harry Frankfurt disagrees with Obama. Discuss.

In the Great Leveller, Walter Scheidel makes the case that in dev countries 1) inequality has risen over last 50 years despite policy, regs etc. Designed to produce equity of opportunity (2) it has only recently reached the levels of 100 years ago but, (3) only major wars, famine, plague have been “great levellers of equality”

“Even in the most progressive advanced economies, redistribution and education are already unable fully to absorb the pressure of widening income inequality before taxes and transfers. Lower-hanging fruits beckon in developing countries, but fiscal constraints remain strong. There does not seem to be an easy way to vote, regulate, or teach our way to significantly greater equality. From a global historical perspective, this should not come as a surprise. So far as we can tell, environments that were free from major violent shocks and their broader repercussions hardly ever witnessed major compressions of inequality. Will the future be different?”

Thus, partly Harry Frankfurt moral philosophical viewpoint is provoking. He distinguishes economic equality with other kinds of inequity and argues that economic inequity is not a moral problem although other kinds are:

“There has recently been quite a bit of discussion—stimulated in part by the publication of the French economist Thomas Piketty’s research—concerning the growth in our society of economic inequality. The size of the gap between the economic resources of those who have more money and those who have less has been increasing rapidly. This development is regarded by many people as deplorable. It is certainly true that those with greater wealth enjoy significant, and often objectionable, competitive advantages over those with less wealth. This is most conspicuous, of course, with regard to consumption. It is also conspicuous, far more importantly, with regard to social and political influence. The richer are in a position to throw around quite a bit more weight than are the poorer, in affecting the character of our social mores and conduct, and in determining the quality and the trajectory of our political life. Insofar as economic inequality is undesirable, however, this is not because it is as such morally objectionable. As such, it is not morally objectionable. To the extent that it truly is undesirable, it is on account of its almost irresistible tendency to generate unacceptable inequalities of other kinds. These unacceptable inequalities, which may sometimes go almost so far as to undermine the integrity of our commitment to democracy, must naturally be controlled or avoided in the light of appropriate legislative, regulatory, judicial, and executive monitoring. It is, I believe, of some considerable importance to get clear about these matters. Appreciating the inherent moral innocence of economic inequality leads to an understanding that it is misguided to endorse economic egalitarianism as an authentic moral ideal. Further, it facilitates recognition of why it may actually be harmful to regard economic equality as being, in itself, a morally important goal. The first part of this book is devoted to a critique of economic egalitarianism. Its conclusion is that, from a moral point of view, economic equality does not really matter very much, and our moral and political concepts may be better focused on ensuring that people have enough. In the second part of the book I will recover one way in which economic equality may indeed be of some moral significance.”

Here are the Amazon links to Schiedel’s Great Leveller and here to Frankfurt's Inequality.

As an aside, it seems both a universal basic income or a job guarantee would meet Frankfurt’s requirements as policy ideas.

ESG plus fundamentals equals alpha

Source: BofAML March 2018

Savita Subramanian (BofAML, Quant team) finds further evidence that investors need to pay attention to ESG. In her 5th note on ESG, she finds ESG is largely uncorrelated with other fundamental factors.

She argues "(see top chart)

2) The proof is in the performance. Adding ESG to a…

· Value strategy (Low forward PE) would have increased returns by 200bps per year (pretty remarkable in a year where Value funds are struggling to maintain a 70bp lead vs. the benchmark).

· Dividend Yield strategy would have added an extra 300bps per year.

· Growth strategy (Earnings Estimate Revision) strategy would have improved returns by 150bps or more per annum."

She further suggests adding ESG to traditional factors would have lowered investors probability of losing money almost across the board (see chart above)

She notes in one of her recent surveys that only a minority of quant funds are using ESG as a signal, even though they are using around 20 signals on average.

This gives me some comfort as a bottom-up fundamental active manager. However, the data is looking increasingly powerful on the quant side as well. There have been positive findings across other ESG data sets (with Sustainalytics and MSCI being the two other most used data sets; this one is the Thomson Reuters data set), although the correlation between these data sets remains relatively poor at between 0.3 to 0.5 in the studies and work I have seen.

The other factor this work and similar raises is the power of passively managed funds. They now make up over 40% of US-dom equity funds up from 20% in 2009, and I do not see this trend changing any time soon. In fact various forces may if anything accelerate this trend.

Vanguard now owns more than 5% of over 494/500 S&P 500 companies. Vanguard is now the steward of many people's capital. That man in the street through Vanguard now owns 1/20th of the largest companies in the US. It will be interesting to see how stewardship evolves in this situation.

More thoughts: My Financial Times opinion article on the importance of long-term questions to management teams and Environment, Social and Governance capital.

One of the best Munger speeches on how to think about a mental model of inversion can be found here.

March 2018 thoughts on greed, fear and risk.

Top selling Drugs

Source: EP Vantage

What’s the length of a patent? 20 years. What’s the social contract behind patents ? Society gives you a time-limited monopoly to incentivise you to invest in R&D and intangibles and enable you to profit at higher levels due to lack of competition.

Drug development takes 8 to 12 years on average, so the average commercial life of a drug based on its first composition of matter patent should run approx 10 years.

Noticeable how many best selling drugs have 20+ years protection. Oft involving long litigation.

One way the pharma industry erodes the social contract is by NOT meaningful innovation and by extending monopolies beyond expectations.

One way it can strengthen trust is by developing life saving medicines and ensuring access.

It’s an active debate what creates more long-term value for shareholders and society.

I’ve written about the history of patents and patent philosophy here.

Original EP Vantage article here

One of the best Munger speeches on how to think about a mental model of inversion can be found here.

If you'd like to feel inspired by commencement addresses and life lessons try: Neil Gaiman on making wonderful, fabulous, brilliant mistakes; or Nassim Taleb's commencement address; or JK Rowling on the benefits of failure. Or Charlie Munger on always inverting; Sheryl Sandberg on grief, resilience and gratitude or investor Ray Dalio on Principles.

Cross fertilise. Read about the autistic mind here.

More thoughts: My Financial Times opinion article on the importance of long-term questions to management teams and Environment, Social and Governance capital.

How to live a life, well lived. Thoughts from a dying man.

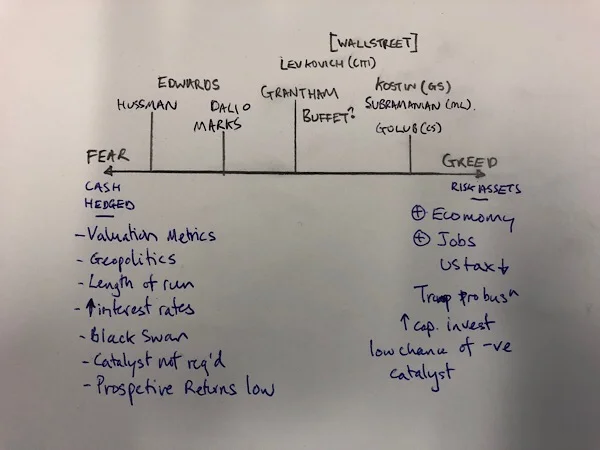

Greed, Fear: plus and minus of the market and thinking on risk Warren Buffet style

A friend asked me about the state of the markets. But, I don’t give advice. That way lies ruin. There’s also complicated regulation. But, you are a professional. The professional system is mostly a relative institutional one. Their view of risk is very different to yours.

Hang on. What’s my view of risk? You’ve spoken to a financial adviser. Yeah, but they are all rubbish. It doesn’t make sense speaking about yields and downsides and tolerance for me.

OK. I can help you think about risk for you. It’s always personal. You are delaying consumption for something today, to allow for greater consumption later (see Warren Buffet 2018 letter). Your risk is you won’t have that consumption later. Thus ensues a conversation over retirement, work, education, children and exactly what we might want to consume later.

Under this view, there’s no point “risking” stuff needlessly, if you have mostly what you want.

Also (again see Buffet, as usual his whole letter worth reading) it made a “purportedly risk-free long-term bond in 2012 a far riskier investment than in stocks” back then for a 2017 pay off. In this case a low return product was a bigger risk for not achieving the goal they wanted.

Finally we got round to markets and we chatted about the range of views being held.

A Fear --- Greed continuum is always in play.

On the fear side:

-Valuation metrics (longer term valuation metrics remain elevated such as Market Cap / GDP and CAPE; see Hussman and here)

-Geopolitics (eg North Korea, Trade wars)

-Length of positive returns in stock market

-Interest rates rising

-Black swans, unknown unknowns

-No catalyst needed for stock market downturns

-Low long term prospective returns from stocks forecast by some

On the greed side:

-Positive economic signals

-positive job signals

-US tax reform

-Trump pro-business rhetoric

-Signs of increased capital investments

-low chance of negative catalysts (eg recession)

Various reasonable experts have different views. Look them up (picture). But remember to focus on what your personal view of risk to achieving your own goals.

One of the best Munger speeches on how to think about a mental model of inversion can be found here.

If you'd like to feel inspired by commencement addresses and life lessons try: Neil Gaiman on making wonderful, fabulous, brilliant mistakes; or Nassim Taleb's commencement address; or JK Rowling on the benefits of failure. Or Charlie Munger on always inverting; Sheryl Sandberg on grief, resilience and gratitude or investor Ray Dalio on Principles.

Cross fertilise. Read about the autistic mind here.

More thoughts: My Financial Times opinion article on the importance of long-term questions to management teams and Environment, Social and Governance capital.

Charlie Munger on GE culture

Charlie Munger is the (older) long time business partner of Warren Buffet, and billionaire investor in his own right. He is Chairman of the Daily Journal Corporation (since 1997) which is legal publishing and software business with a portfolio of investments on the side. The AGM serves as a Q&A of Charlie Munger wisdom more than a scrutiny of the Daily Journal business. The business itself is in the $40m sales range, so not large in the world of big business.

These are some comments from his recent AGM.

On GE and on culture: “what caused the failure of performance at General Electric? …part of it I would say, is the system at General Electric where you rotate executives through so different assignments as if they were so many army officers, building up a resume to see if they can become Generals. I don’t think that works as well as keeping people in one business for a long time and having them identify with the business, the way Berkshire does….”

"... How can an outsider really know a company’s culture? And then finally how do you go about assessing the culture of a company like General Electric..,

…you understand culture best where it’s really dominant. So for a place like Costco, and there the culture is a vast and constructive force. And it will probably continue for a very, very, long time. And then you get into General Electric, part decentralized, partly not. And it gets very complicated. What is the culture of General Electric? The businesses can be so radically different.

Maybe headquarters can have a certain kind of culture. .... And I do think it’s, there are very few businesses like Costco that have a very extreme culture ... basically one big business all the way.

And I love a business like Costco, because of the strong culture and how much can be achieved if the culture is great. But the minute you get into bigger and more complicated places, I mean can you talk about the culture of General Motors, or the culture of AT&T, it’s a very difficult subject.

What big businesses have in common is that they get very bureaucratic. That’s the one norm in culture is they get very bureaucratic. And this happens to the government too. Big governmental bodies. I don’t like bureaucracy. I mean it fixes a lot of errors, I don’t have any substitute for it though. But I don’t personally like big, bureaucratic cultures. I don’t think very much about big bureaucratic cultures.

I don’t know how to fix bureaucracy in a big place. I would regard it as a sentence to hell if they gave me some company with a million employees and told me to change the culture. I mean it’s hard to change the culture in a restaurant. If a business is already bureaucratic, how do you make it un-bureaucratic? It’s a very hard problem..."

On banks: "Banking is a very peculiar business. The temptations that come to a banking CEO are way, the temptations to do something stupid are way bigger in banking than they are in most businesses. Therefore it’s a dangerous place to invest. There are a lot of ways in banking to make your near term future look good by taking risks you really shouldn’t take for the sake of your longer term future. And so banking is a dangerous place to invest, and there are few exceptions. And Berkshire tries to be in the exceptions, as best it could. And I have nothing more to say on that subject except, I’m sure I’m right.”

On investing: "...the first rule of fishing is fish where the fish are. And the second rule of fishing is don’t forget the first rule. And investing is the same thing. Some places have lots of fish, and you don’t have to be that good a fisherman to do pretty well. Other places are so heavily fished that no matter how good a fisherman you are, you’re not going to do very well.

And the world we’re living in now, an awful lot of places are in the second category.

I don’t think that should discourage anyone. I mean life’s a long game and there are easy stretches and hard stretches and the younger generation has opportunities. And the right way to go through life is to take it as it comes and to do the best you can. And if you live to an old age, you’ll get your share ..."

"Thoughts on the valuation of software companies like Apple, Facebook, Google, Amazon, Alibaba. Are they overvalued, potentially undervalued, too early to tell?

Well my answer is I don’t know. Next question. "

Full transcripts available here. One of the best Munger speeches on how to think about a mental model of inversion can be found here.

If you'd like to feel inspired by commencement addresses and life lessons try: Neil Gaiman on making wonderful, fabulous, brilliant mistakes; or Nassim Taleb's commencement address; or JK Rowling on the benefits of failure. Or Charlie Munger onalways inverting; Sheryl Sandberg ongrief, resilience and gratitude or investor Ray Dalio on Principles.

Cross fertilise. Read about the autistic mind here.

More thoughts: My Financial Times opinion article on the importance of long-term questions to management teams and Environment, Social and Governance capital.